The third quarter of 2024 saw an increase in stablecoin usage and adoption, according to the Q4 Guide to Crypto Markets report from Coinbase with Glassnode.

Stablecoins reached a record market capitalization of nearly $170 billion in the third quarter of 2024, according to the report. This growth occurred alongside the implementation of new European Union regulations on crypto-asset markets, which introduced clearer rules for stablecoin operations.

Stablecoins have become a key tool for users looking for faster, cheaper and more secure transactions. Their utility in payment systems, including remittances and cross-border transfers, has continued to expand.

Recently, Anthony Pompliano argued that technological innovations outside of crypto could lead to a new era in which stablecoins become the primary means of transaction in a machine-driven economy. This increased adoption reflects the growing role of stablecoins in crypto trading and real-world financial systems.

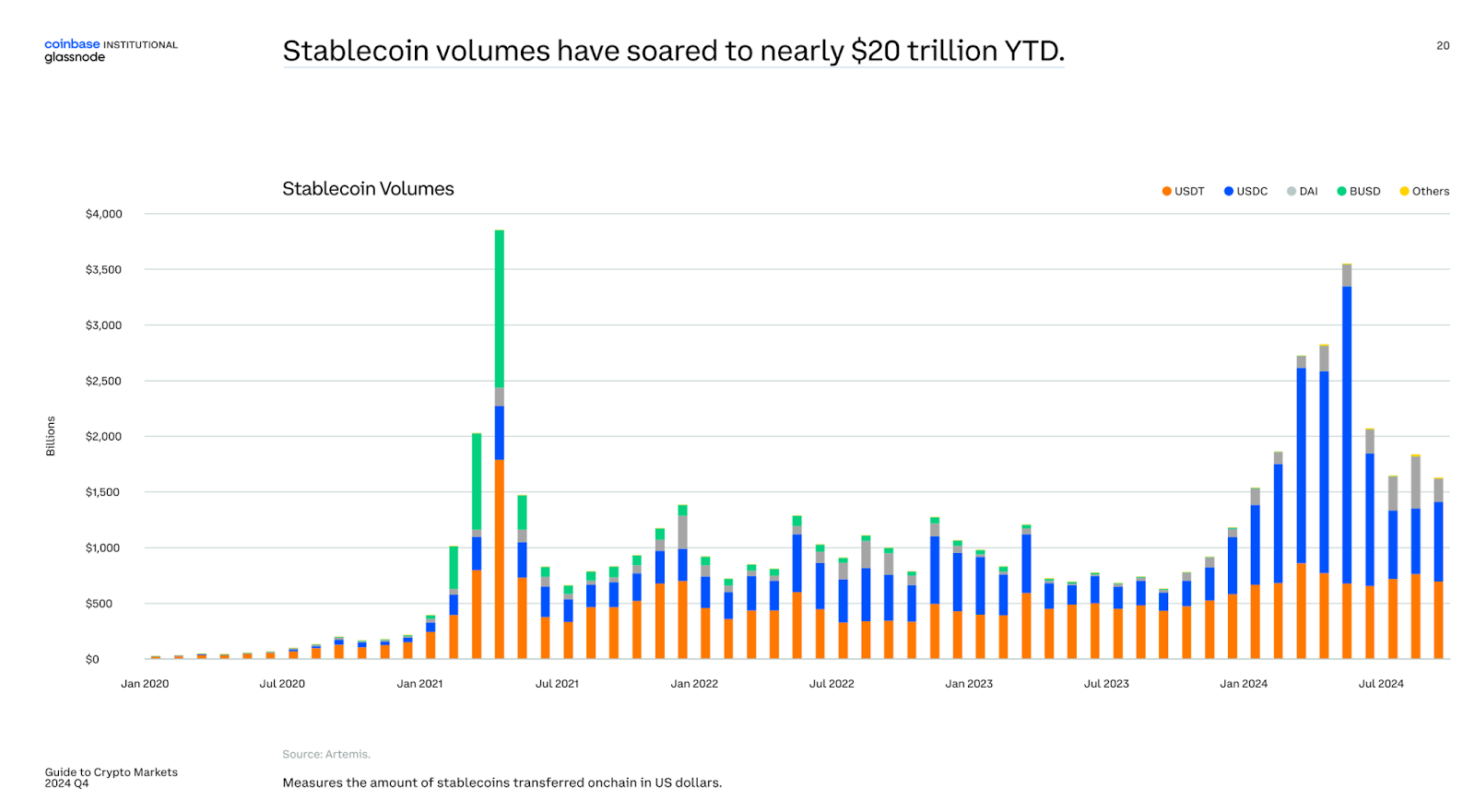

According to the report, stablecoin volumes reached nearly $20 trillion year-to-date in the third quarter, indicating their growing role in the global economy.

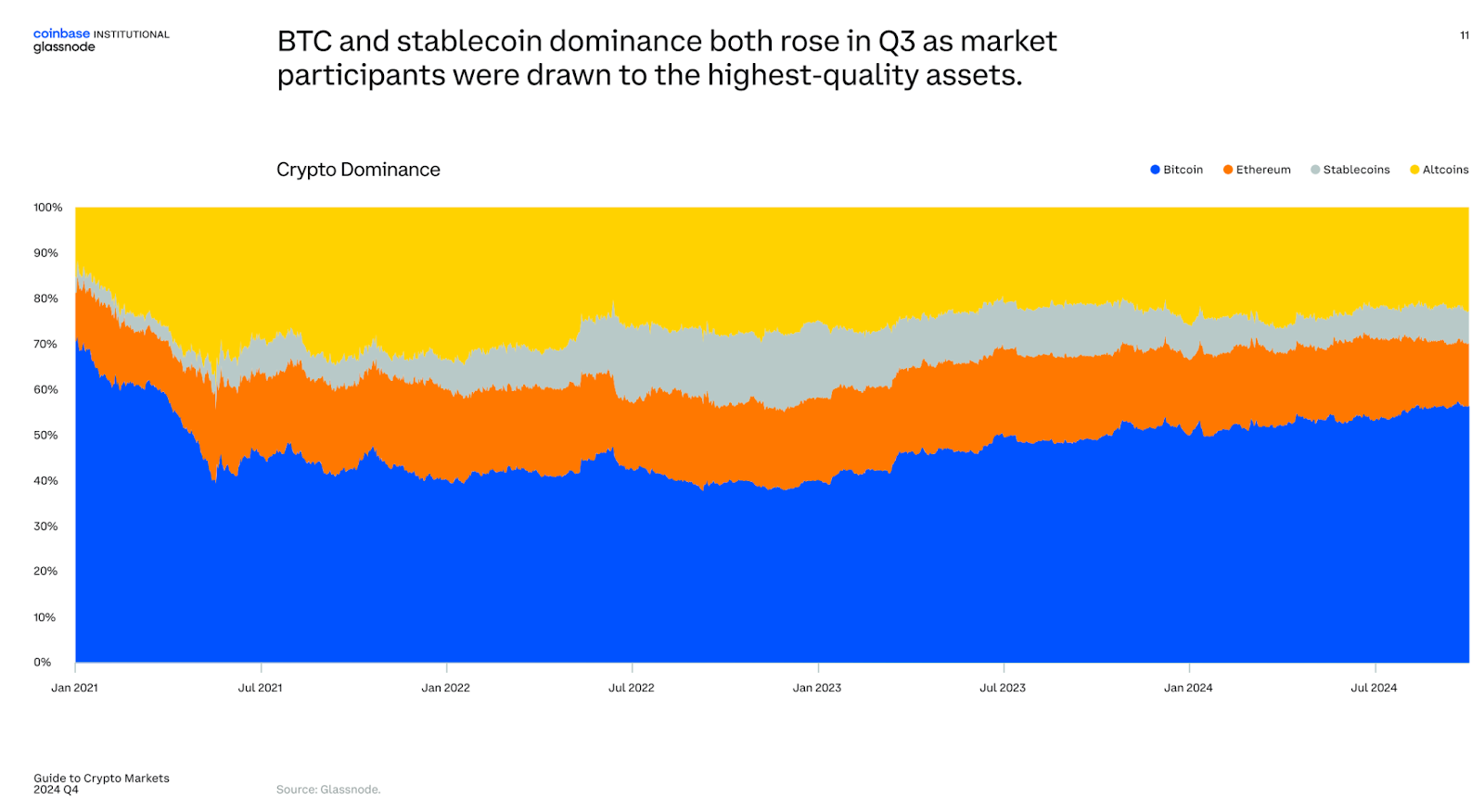

Domination of Stablecoin and Bitcoin

Stablecoin’s dominance also increased in the third quarter alongside Bitcoin (BTC), with crypto investors turning to what they view as the highest quality digital assets.

The current BTC cycle closely follows the 2015-2018 and 2018-2022 cycles, which ended with returns of almost 2,000% and 600%, according to the report.

What is MiCA?

Cryptoasset Markets Regulation is a comprehensive framework adopted by the European Union in June 2023 to regulate the crypto industry in its 27 member countries. It opens a transition period of 12 to 18 months for the implementation of rules on anti-money laundering, combating the financing of terrorism and the custody of digital assets, among others.

MiCA’s impact on stablecoins remains to be seen, but Tether (USDT) CEO Paolo Ardoino expressed concern that MiCA’s 60% cash reserve requirement for stablecoins could create systemic risks for European banks. He argued that such regulations could exacerbate liquidity problems during large-scale buyouts, potentially leading to bank failures.